Vanilla Buy-to-Let vs. HMO Conversion: How to Unlock Double-Digit Yields

12/22/20254 min read

Understanding Buy-to-Let and HMO Investments

Buy-to-let (BTL) properties and Houses in Multiple Occupation (HMOs) represent two distinct strategies within the real estate investment sector, each carrying its own specific attributes and regulatory frameworks. A buy-to-let property is typically a residential property rented out to a single tenant or family, providing a straightforward rental income stream. This model generally adheres to fewer regulatory requirements, making it a popular choice for novice landlords. Conversely, an HMO is defined as a property that is rented to three or more tenants who are not from the same household and who share facilities such as bathrooms and kitchens. Due to the shared nature of these facilities, HMOs are subject to stricter licensing and regulatory conditions, requiring landlords to meet higher safety and quality standards.

The appeal of buy-to-let investments often lies in their simplicity and predictability; landlords can expect a consistent monthly rent from tenants living in separate households. Meanwhile, HMOs have gained popularity due to their potential for generating higher yields. With multiple tenants occupying a single property, landlords can effectively increase their rental income, which is particularly appealing in high-demand urban areas where rental rates may exceed traditional single-family homes.

Landlords considering the transition from standard buy-to-let properties to HMO conversions should be aware of the unique challenges and benefits associated with HMOs. While the higher rental yields can be enticing, they also come with additional responsibilities, from ensuring compliance with property regulations to management complexity. Understanding these fundamental differences equips aspiring landlords with the necessary knowledge to make informed investment decisions, paving the way for a numerical comparison of potential returns and risks involved in each investment type.

The Financial Impact: A Side-by-Side Comparison

When evaluating the financial implications of property investment, particularly in the context of rental income potential, it is essential to consider both Vanilla Buy-to-Let (BTL) and Houses in Multiple Occupation (HMO) conversion models. These two approaches can significantly differ in terms of rental yield and overall cash flow.

For instance, a typical 3-bedroom house under the Buy-to-Let scheme would generate a monthly rental income of approximately £900. This figure is relatively stable, catering to families or professionals seeking long-term tenancies. The expenses associated with a BTL property can include mortgage repayments, maintenance costs, insurance, and property management fees. However, the predictable nature of this income stream often allows landlords to manage their expenses more effectively.

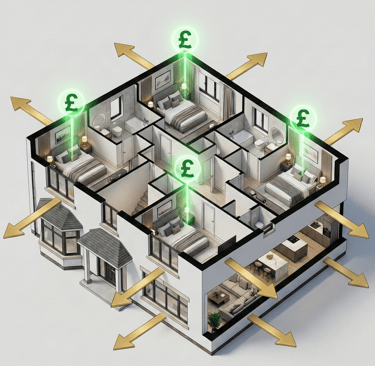

In contrast, converting the same 3-bedroom house into a 5-bedroom HMO has the potential to unlock substantially higher rental income, with projections estimating around £2,500 per month. This increased cash flow arises from renting individual rooms to multiple tenants, typically young professionals or students, who may prefer shared accommodation for its affordability and social aspects. While the enhanced income potential is appealing, landlords must also account for various associated costs with the HMO model, including higher maintenance demands, additional regulatory compliance, and potentially increased utility costs.

Ultimately, these financial calculations reveal the stark differences between the two approaches. While a Vanilla Buy-to-Let strategy offers reliability and lower risk, the HMO model presents an opportunity for significant revenue generation. Investors must weigh these advantages against the implications of managing multiple tenants and increased operational responsibilities. Understanding the financial impact of each strategy is crucial in making an informed decision that aligns with individual investment goals.

Maximizing Rental Yields: Benefits of HMO Conversion

Investing in Houses in Multiple Occupation (HMOs) can significantly maximize rental yields compared to traditional buy-to-let properties. One of the primary advantages of HMO conversions lies in the potential for higher income due to multiple rent payments from various tenants. This structure enables landlords to achieve double-digit yields more consistently, as the overall rental income is typically higher than that generated by a single family unit.

Moreover, HMO conversions offer landlords greater control over tenant selection. By allowing flexible lease arrangements, landlords can choose individuals for shared accommodations who are more likely to pay their rent consistently and contribute to a harmonious living environment. This is particularly beneficial in locations with high demand for rental accommodations, where tenants may be looking for affordable or shared living spaces.

Reduced vacancy rates are another advantage of HMO conversions. Since these properties accommodate multiple tenants, a landlord is less likely to experience significant income loss during transition periods. Even if one room remains vacant, the remaining occupants can continue to provide a steady stream of income. This safety net can prove invaluable during economic fluctuations when market demands may shift unexpectedly.

Location plays a crucial role in enhancing the profitability of HMO conversions. Properties situated near universities, businesses, or transport links tend to attract higher tenant interest, making them prime candidates for generating lucrative rental yields. Effective property management, encompassing regular maintenance and communication with tenants, can further enhance the reputation of an HMO, ensuring occupancy consistency.

Adopting a 'rent high' strategy allows landlords to maximize their financial returns. By understanding local market dynamics, setting competitive but attractive rents, and catering to tenant needs, landlords can secure substantial yields while maintaining occupancy levels. Overall, HMOs represent a compelling opportunity for landlords looking to expand their rental portfolio with dual benefits of high returns and financial resilience.

Conclusion and Call to Action: Unlock Your Property’s Potential

Throughout this blog post, we have explored the differences between vanilla buy-to-let properties and House in Multiple Occupation (HMO) conversions. Each investment strategy offers unique advantages; however, the potential for securing double-digit yields is notably greater with HMO conversions. This is particularly significant for landlords who are aiming to maximize their return on investment in a competitive rental market.

HMO conversions allow property owners to rent out individual rooms to multiple tenants, significantly increasing the rental income in comparison to traditional buy-to-let models. As discussed, this approach not only provides greater financial rewards but also aligns with the growing demand for affordable housing solutions. Landlords must consider their specific properties and evaluate their potential for HMO conversion, taking into account local regulations and market conditions.

Now is the time for landlords to assess their portfolios and strategic options. Transitioning from a vanilla buy-to-let to an HMO can unlock substantial financial possibilities and enhance overall yield stability. Moreover, by understanding the intricacies and benefits of both investment strategies, property owners can make informed decisions that align with their financial goals.

To assist in this transition, we invite you to request a free yield simulation for your current property. This simulation can provide vital insights into the financial implications and potential returns of converting your property into an HMO. Understanding the dynamics of yield potential is crucial for any landlord looking to optimize their investment. Take action today to uncover the financial opportunities your property may contain.

Investing

Maximize profits with our expert guidance.

Services

Support

info@goldenestateinvestments.com

(+44)01212855107

© 2025. All rights reserved.